By Janus Boye

Jörg Schäffer is a long-time part of our community and also leads our product management groups in Germany and Switzerland

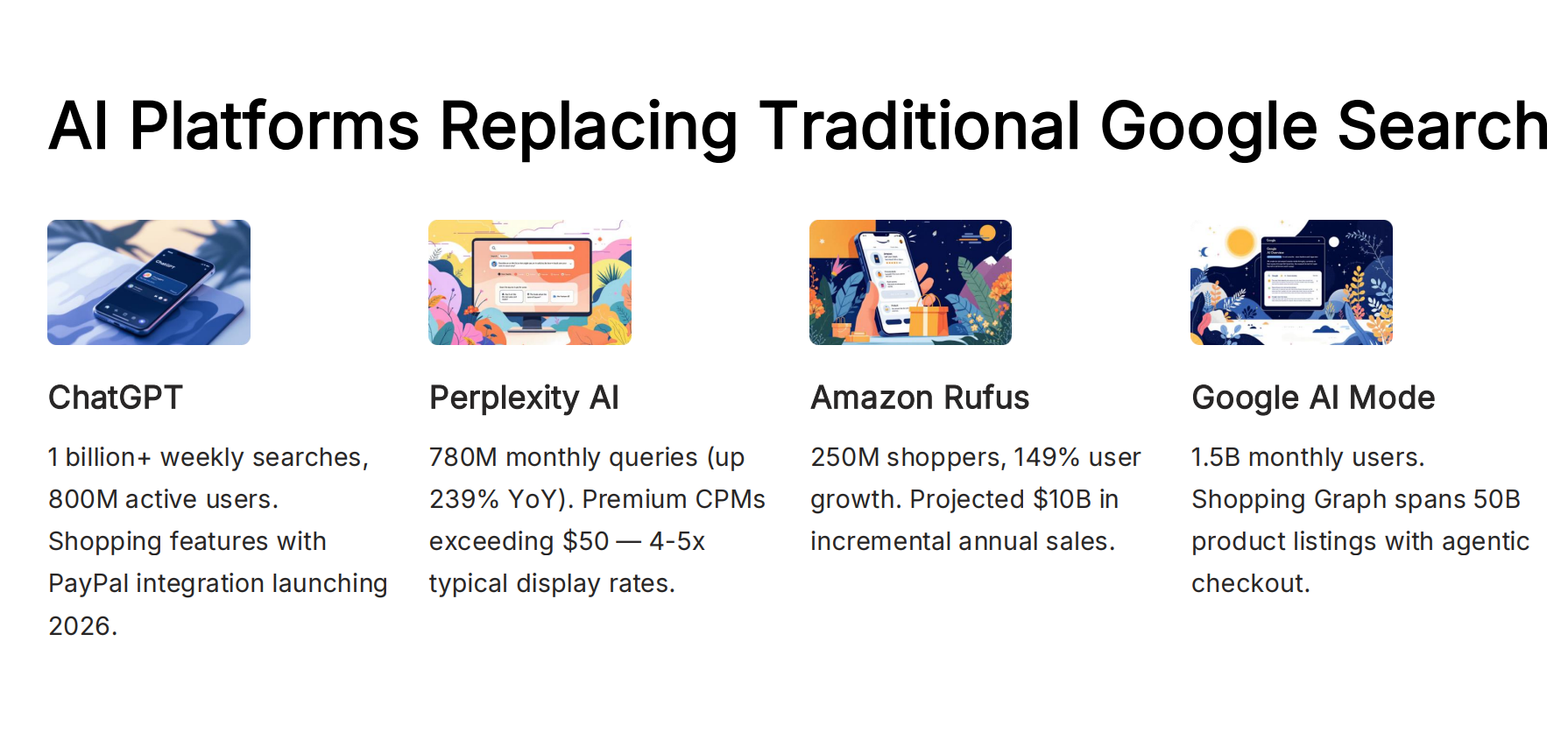

The traffic collapse is real. Around 800 million weekly users of ChatGPT are already changing how people search, alongside growing audiences for Gemini, Perplexity and other AI services. With more than half of all searches now ending without a click, some organisations are experiencing traffic losses of up to 90%.

These are no longer edge cases or future warnings. Over the past year, AI-generated answers have started to satisfy user intent before visitors ever reach a website, fundamentally changing how visibility, authority and value are created online.

In last week’s end-of-year member’s call, we explored what this shift really means in practice with Jörg Schäffer, a Hamburg-based product management and product marketing leader with nearly two decades of experience working at the intersection of content platforms, search and digital commerce. Jörg shared his perspective on the rise of Generative Engine Optimisation (GEO), the growing influence of AI platforms, and the emerging content arms race that is reshaping how organisations are discovered.

What emerged clearly from the discussion was this: the decline of website traffic is not a temporary disruption. It is a structural change that demands a new way of thinking about digital strategy.

The traffic collapse is already happening

For years, declining organic traffic was something many teams could explain away with algorithm updates or seasonal changes. That excuse no longer holds.

How to get found on ChatGPT was the topic of another member’s call back in July

AI-generated answers are now satisfying user intent before visitors ever reach your website. Zero-click searches account for roughly 58–69% of Google queries, and when AI Overviews appear, click-through rates can drop by 34–61%. In extreme cases, publishers have lost almost all of their traffic and been forced to shut down entirely.

This is not a future scenario. It is already reshaping how people discover, evaluate and buy.

As Jörg put it during the session, the web’s long-standing value exchange, content in return for traffic, is breaking down.

From search rankings to machine recognition

A slide from the presentation - click to expand

For years, digital visibility followed a relatively stable logic. If your pages ranked well in search engines, users would click through, spend time on your site and, with some luck, convert.

AI-driven search changes that logic at a more fundamental level. Instead of presenting users with a list of links, these systems synthesise answers from many sources and present a single, confident response. In doing so, they often remove the need to visit any individual website at all.

In this environment, success depends less on how well a page is tuned for search engines and more on whether an organisation is recognised, trusted and clearly understood by machines. Being technically accessible still matters, but it is no longer sufficient on its own.

What many teams are now grappling with is the shift from optimising for clicks to optimising for inclusion. The goal is not simply to appear somewhere in a list of results, but to be considered credible enough to be referenced when an AI constructs its answer.

That has far-reaching implications. Reputation across the wider web becomes more important than tactics on individual pages. Clear structure and consistency matter more than clever copy. And authority is increasingly established outside an organisation’s own digital properties, through mentions, discussions and signals that sit beyond direct control.

As Jörg noted during the call, only a small proportion of the sources referenced by AI-generated answers come directly from brand-owned websites. Most visibility is earned elsewhere.

The uncomfortable implication is that organisations can no longer optimise their way out of this challenge from within their own site alone.

The rise of AI platforms as intermediaries

A slide from the presentation - click to expand

Search behaviour is fragmenting across a growing number of AI-driven platforms.

Tools such as ChatGPT and Perplexity increasingly act as starting points for research and decision-making, while Amazon’s AI assistants shape product discovery within its own ecosystem. Google is embedding AI answers directly into search results, further reducing the need for users to click through to individual websites.

Each of these platforms inserts itself between organisations and their audiences. Even when a brand is selected as a source, the interaction often remains within the AI interface rather than moving on to the organisation’s own channels.

This creates a new dependency. Visibility may increase, but direct relationships become harder to establish and measure.

The content arms race has begun

Behind the scenes, this shift has triggered a new kind of arms race.

AI companies are aggressively harvesting content from across the web, often ignoring traditional signals of consent. Today, a significant share of high-traffic websites are being accessed by AI bots, while only a small minority actively block them. New generations of scrapers increasingly behave like real users, making detection and prevention difficult.

The largest publishers are already striking licensing deals worth hundreds of millions, securing both revenue and preferential access. Smaller organisations face a tougher trade-off between protecting their content and remaining visible.

As several members observed during the call, there are few stable rules to rely on. Unlike traditional search optimisation, this environment is still forming, volatile and unevenly governed.

What digital teams should do now

Despite the uncertainty, the discussion converged on a small number of practical priorities.

Organisations need to invest in authority beyond their own websites, recognising that visibility in AI answers is driven by reputation across the wider web. They also need to strengthen their technical foundations, ensuring that content is well structured, consistent and easy for machines to interpret. Finally, they need to rethink how success is measured, moving beyond traffic and rankings towards a clearer understanding of how, where and whether they appear in AI-generated answers.

Industry analysts expect spending on optimising for AI-driven discovery to outpace traditional search optimisation significantly over the coming years. The transition is already under way.

Adapt or disappear

The end of website traffic does not mean the end of digital strategy. But it does mark the end of treating traffic as the primary indicator of success.

The organisations that thrive next will be those that accept a harder truth: the website is no longer the centre of the digital universe. Authority, relevance and trust are now distributed across platforms, systems and conversations that sit well beyond a single domain.

The question is no longer whether this shift is happening.

It is whether your organisation is adapting fast enough.

Learn more and prepare for 2026

This post is based on a Boye & Co end-of-year member’s call with Jörg Schäffer. If you want to go deeper, the full slide deck (PDF) from the session is available, and the entire recording is published on YouTube.

Looking ahead to 2026, we will continue to explore this shift and its wider implications. Several member organisations are already seeing early signals. Jonathan Healey, Group Technology Director at IDHL in Leeds, for example, reports traffic declines across client sites, alongside improving conversion rates. One possible explanation is that AI-driven search reduces overall volume while sending visitors who are more clearly intent-driven, effectively filtering users before they reach the website.

At the same time, this picture is likely to evolve. As major platforms introduce direct shopping capabilities, such as OpenAI’s experiments with Stripe and PayPal-based checkout, pressure on ecommerce margins is likely to increase. Google also enters this phase with a significant structural advantage, having long controlled large volumes of high-quality product data through Google Shopping.

A cautious working hypothesis is that sellers of largely interchangeable, commodity products may feel this pressure first, while brands offering premium or experience-led products may be less immediately affected. Publishers, by contrast, appear most exposed, as their website is often the destination itself, and increasingly one that users never reach.

As with many of our recent discussions, this session raised more questions than it answered. That feels appropriate. We are still early in this transition, and much of what will matter in 2026 will be shaped by how organisations respond now, through experimentation, capability building and shared learning across the community.

The conversation naturally continues in our peer groups at conferences across Europe and North America. You are very welcome to join us and be part of it.